")

15.07.2020

On January 1st, 2020, the " Law for the Protection against Manipulation of Digital Basic Records" came into force. Hereby, the obligation to keep individual records for electronic cash register systems was tightened again.

With the "Principles for the proper keeping and storage of books, records and documents in electronic form and for data access" (GoBD for short), strict specifications for electronic cash register systems were already established in 2017. With a deadline of 01.01.2020, the legislator has now tightened these requirements once again. The aim here is to prevent subsequent manipulation of the recorded cash transactions and the associated tax evasion.

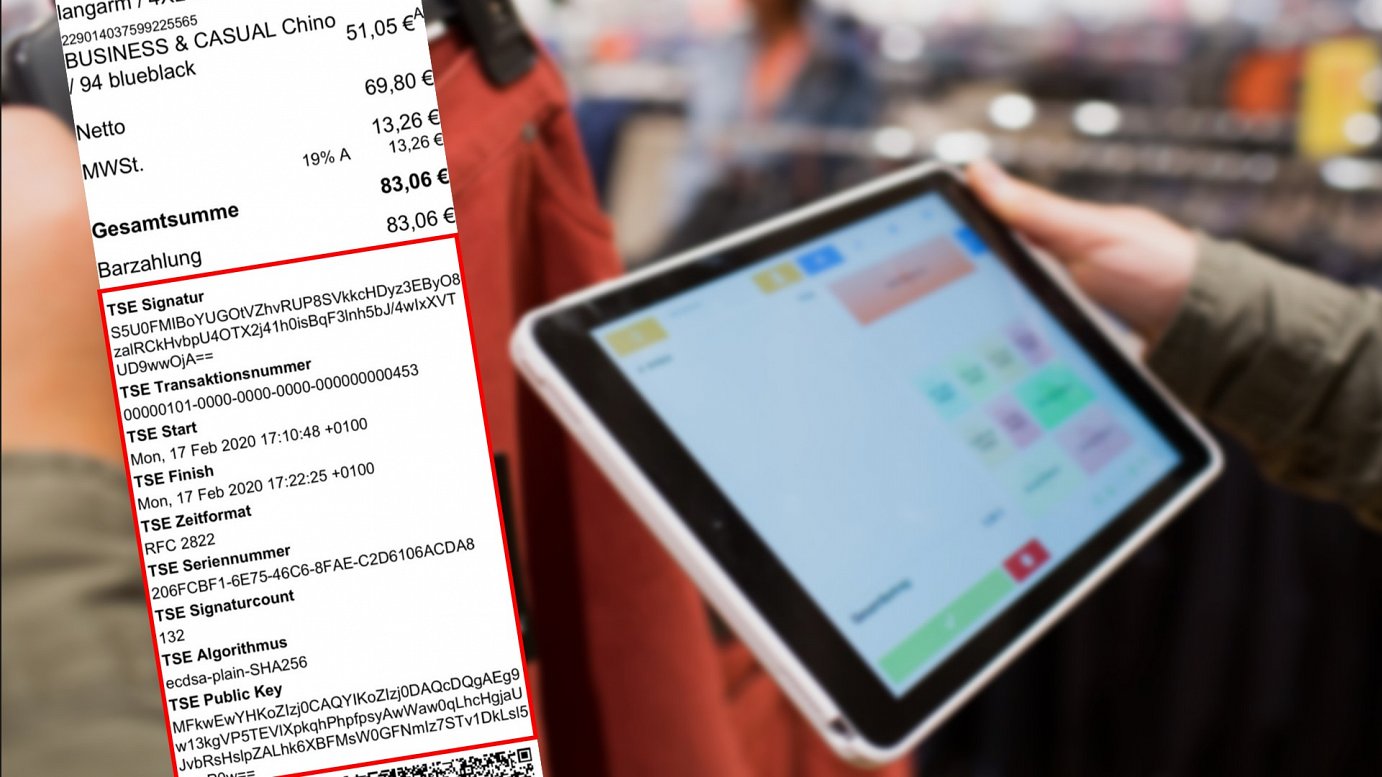

Starting this year, electronic recording systems must have a certified technical security device consisting of three components:

- Security module: The security module ensures that cash register entries are logged at the start of the recording process and cannot be changed later without being detected.

- Storage medium: The individual records are stored on the storage medium for the duration of the statutory retention period.

- Unified digital interface: The digital interface is intended to ensure smooth data transmission, for auditing purposes.

The technical security device with which the records of the POS system are to be secured at the start of the recording process must be certified in accordance with the specifications of the German Federal Office for Information Security (BSI). However, there is no such certification requirement for the POS system. This must only have an interface to a certified security device. Even though the new law came into force on 01.01.2020 and therefore applies de facto to all electronic cash register systems, the absence of a technical security device should not be objected to by the tax office until 01.10.2020. A corresponding order was issued by the Federal Ministry of Finance (BMF) on 05.11.2019.

In recent days, seven states have already announced that their tax authorities will extend this deadline of non-objection due to Covid-19 to March 31, 2021, if the company can prove,

- that the TSE has been bindingly ordered from a qualified cash register manufacturer

or

- that the implementation of a cloud-based TSE is planned, but that this is demonstrably not yet available for the company.